Philippine Airlines (PAL) has forged a partnership with All Nippon Airways (ANA) in one of the first moves by the Philippine carrier since Lucio Tans LT Group regained control in Sep-2014. The new codeshare should significantly improve PALs position in Japan, the airlne's largest international market.

But the deal does not indicate a shift in strategy for PAL, which had been under control of Philippine conglomerate San Miguel since Apr-2012. The codeshare only covers the Philippines-Japan market and domestic connections in each country.

PAL needs stronger partnerships as well a much larger portfolio of codeshares. PAL particularly needs a partner for the US market with ANA a potential suitor.

PAL is instead moving forward with a risky plan to launch service in its own right to New York.

ANA and PAL will begin codesharing on 26-Oct-2014

PAL chairman and CEO Lucio Tan announced on 1-Oct-2014 a codeshare partnership with ANA CEO Osamu Shinobe. The two-way codeshare will be implemented on 26-Oct-2014 and cover all 74 weekly flights operated by the two carriers between the Philippines and Japan.

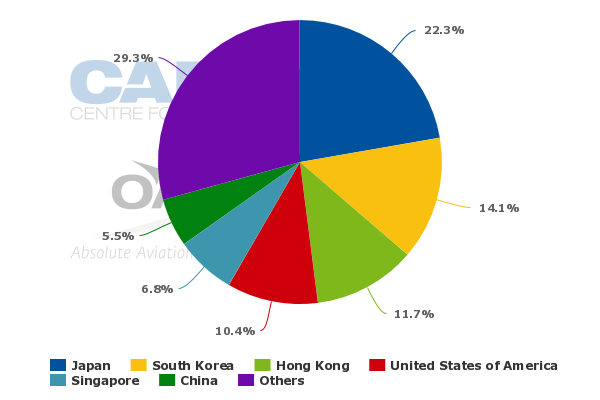

Japan is a strategically important market for PAL and currently accounts for about 22% of the carriers total international seat capacity. It is PALs largest single market based on seats. On an ASK basis only the US is a larger market.

Philippine Airlines international capacity share (% of seats) by country: 29-Sep-2014 to 5-Oct-2014

But competition between the Philippines and Japan has intensified significantly over the past year, driven primarily by expansion at PAL rival Cebu Pacific Air. Forging a partnership with ANA is a sensible strategic response by PAL as it will help PAL maintain and leverage its leading position in the Philippines-Japan market.

PAL currently operates eight daily flights to Japan, including four to Tokyo Narita and one each to Tokyo Haneda, Fukuoka, Osaka, Nagoya. All the flights operate from PALs main hub at Manila except two flights from Cebu to Narita. PAL uses a mix of A320s, A321s and A330s on flights to Japan with larger aircraft often being deployed during peak periods.

PAL is planning to increase Manila-Haneda to 11 weekly flights in late Oct-2014, giving it 60 weekly frequencies to Japan when the codeshare with ANA is launched. ANA currently has 14 weekly flights to the Philippines, including seven 787-8 frequencies from Narita to Manila and seven 787-8 frequencies from Haneda to Manila.

ANA and PAL routes between the Philippines and Japan: as of Oct-2014

PAL and ANA will control two-thirds of the Philippines-Japan market

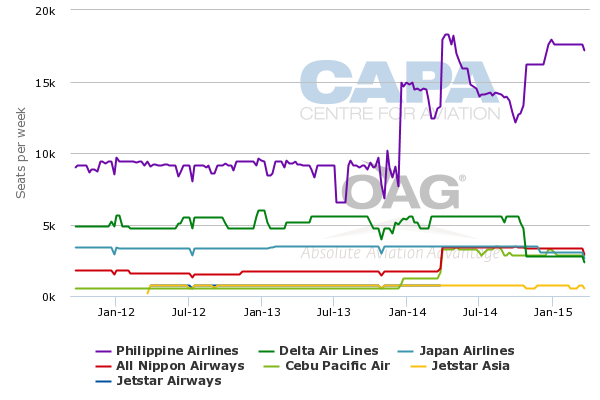

Combined, the two carriers will account for a powerful 67% share of point-to-point capacity between the Philippines and Japan based on CAPA and OAG data for Nov-2014. The remaining 33% is split between four carriers including Japan Airlines (JAL) with about 12%, Cebu Pacific with 10%, Delta Air Lines with 9% and Jetstar Asia with 3%.

Philippines to Japan capacity by carrier (one-way seats per week): 19-Sep-2011 to 29-Mar-2015

JAL currently operates two daily flights from Narita to Manila while Cebu Pacific has 16 weekly flights to Japan, including seven on Manila-Narita, five on Manila-Osaka and four on Manila-Nagoya. JAL has more total capacity in the Philippines-Japan market as it uses 767s while Cebu Pacific uses A320s.

All but three of Cebu Pacifics 16 weekly flights have been added over the past year. Cebu Pacific was blocked until 2H2013 from expanding to Japan beyond its longstanding three weekly flights to Osaka because of Japanese Civil Aviation Bureau (JCAB) restrictions on Philippine carriers.

Japanese authorities lifted these restrictions, which had for five years prevented all Philippine carriers from adding any flights to Japan, in 2013 after Philippine authorities passed an ICAO audit. The two countries also agreed in Sep-2013 to an expanded air services agreement, enabling significant expansion for Philippine carriers.

See related report: Cebu Pacific, AirAsia Zest, Tigerair and Philippine Airlines race to add flights to Japan

Foreign carriers benefitted from the prior JCAB restrictions on Philippine carriers, including airlines holding fifth freedom rights between the Philippines and Japan. Jetstar Asia currently operates four weekly A320 flights from Manila to Osaka which originate in Singapore (and is seeking more). Delta Air Lines currently operates one daily 747-400 flight from Manila to Narita and one daily 747-400 flight from Manila to Nagoya, according to OAG data.

LCC competition changes dynamic of Philippines-Japan market, including squeezing Delta Air

Delta has decided to drop its Manila-Nagoya flight at the end of Oct-2014, which will reduce Deltas total share of capacity in the Philippines-Japan market from about 19% to about 10%. Deltas Manila-Nagoya flight continues on to Detroit but relies heavily on local traffic. Delta also carries local passengers between Manila and Tokyo but the portion of fifth freedom traffic is much higher on Manila-Nagoya because Delta has a hub in Narita while it only offers one connection to the US mainland from Nagoya.

(In addition to Detroit, Delta serves Honolulu and Guam from Nagoya but Honolulu and Guam would be less appealing to Manila passengers as PAL operates non-stop flights in the Manila to Honolulu and Guam markets. Delta will still be able to compete in the Manila to Detroit, Honolulu and Guam markets by using its Manila-Narita service. Delta will likely end up carrying fewer local passengers between Manila and Narita as Manila-Nagoya is dropped but such a trade off is a positive given the new LCC competition in the Manila-Tokyo market.)

Delta clearly benefitted from the lack of competition in the Manila to Nagoya and Tokyo markets due to the JCAB restrictions. With Cebu Pacific now serving Manila-Nagoya the route is no longer viable for Delta given Deltas much higher cost structure. Delta would also be aware that LCC competition between Philippines and Japan is expected to further intensify as Cebu Pacific considers adding more capacity to Japan and as the AirAsia Groups Philippine affiliate prepares to enter the market.

PAL also has been impacted by the new LCC competition in its largest market. But it has a lower cost structure than Delta and strategically cannot afford to reduce its presence. PAL instead has been increasing capacity to Japan following the lifting of JCAB restrictions and the new air services agreement, which in addition to increasing the total capacity, has for the first time authorised flights to the Philippines from Haneda.

PAL was able to secure all 14 weekly traffic rights available to Philippine carriers in the Haneda-Manila market. PAL launched double daily Haneda flights at the end of Mar-2014 but quickly pulled back to seven weekly flights due to a lack of demand.

The new partnership with ANA should help PAL improve its performance on the Haneda route as PAL adds back four weekly flights for a total of 11. PAL will likely look to add back the other three weekly flights as it risks losing some of its Haneda rights to Cebu Pacific.

PAL gains access to Japanese domestic market with the ANA codeshare

The partnership with ANA is particularly important for the Haneda route as Haneda is ANAs main domestic hub. The new ANA-PAL codeshare gives PAL access to 11 secondary destinations in Japan. While some of these destinations will also be available from Fukuoka, Nagoya, Osaka and Narita, Haneda will be the main connection point for PAL passengers.

Domestic connections should enable PAL to maintain and potentially grow its position in Japan despite the intensifying LCC competition. Access to behind gateway secondary markets will be a differentiator for PAL and enable it to work more closely with Japanese agents based in the 11 cities served through the new codeshare. Japan is a large and growing source market for the Philippine tourism sector but a large portion of Japanese travellers are from secondary cities.

ANA domestic routes included in ANA-PAL codeshare

ANA meanwhile will benefit from the codeshare as it will get access to 10 domestic destinations that are served from Manila by PAL or its full-service regional subsidiary PAL Express. The main tourist destinations in the Philippines are covered by the codeshare such as Caticlan, Kalibo and Puerto Princesa. (Caticlan and Kalibo are gateways for the popular resort island of Boracay while Puerto Princesa is on the resort island of Palawan.)

For Japanese passengers Manila is primarily a business destination, which is the main focus for ANA. But ANA could use the domestic connections to boost economy class loads as well as gain access to cities such as Cebu and Davao where there is also some business traffic.

PAL and PAL Express domestic routes included in ANA-PAL codeshare

The partnership should also improve ANAs presence in the Philippine market from a local point of sales perspective as ANA is a relative newcomer to the Philippines. ANA launched services to Manila from Narita in Feb-2011 and added its Haneda-Manila service at the end of Mar-2014.

The PAL-ANA codeshare adds another relatively limited partnership for PAL

The ANA-PAL partnership however does not include international markets beyond the Philippines or Japan. ANA would not have much of a need to use PAL beyond Manila as it already codeshares with other Southeast Asian carriers including Garuda and Singapore Airlines. But PAL has a very limited portfolio of partners and could benefit from international connections beyond Tokyo.

According to OAG data, PAL currently codeshares with eight carriers Air Macau, Cathay Pacific, Emirates, Etihad Airways, Garuda Indonesia, Gulf Air, Malaysia Airlines and Vietnam Airlines. ANA will become its ninth codeshare partner but only briefly as PAL and Emirates are now in the process of terminating their partnership, which is limited to the Manila-Dubai route.

PALs partnerships are all limited to flights between the hubs of each carrier and domestic connections. In several cases, such as with Cathay Pacific, domestic connections are not even included. (Cathay Pacific is a major competitor to PAL on Manila-Hong Kong and in the Philippines-US market but the two codeshare on Cebu-Manila.)

Even the expanded partnership forged earlier this year between PAL and Etihad only includes PAL-operated domestic connections as well as flights operated by both carriers between Manila and Abu Dhabi. Flights beyond Abu Dhabi are not included at least for now.

PAL currently does not have any codeshares to Europe or North America or within either of these markets. This is a huge gap that has become more pressing given PALs resumption of services to Europe and expansion in the US.

PAL so far has seemed keen to cover these markets on it own. New York is the latest example of PAL being potentially over-ambitious with its own metal.

PAL will launch New York but still lacks a US partner, although Canada-US fifths help

PAL announced on 30-Sep-2014 plans to launch services to New York JFK on 15-Mar-2015 with four weekly A340-300 flights via Vancouver. PAL currently serves Vancouver daily with three of the seven frequencies continuing on to Toronto.

As New York is introduced, PAL will increase Vancouver to 11 weekly flights and also increase Toronto to four flights, leaving three turnaround flights. PAL has fifth freedom rights from US and Canadian authorities to carry passengers between Vancouver and New York.

PAL is keen to expand in the US market as for several years it was prevented from adding capacity or new destinations in the US due to the Philippines Category 2 safety rating.

The FAA upgraded the Philippines to Category 1 in Apr-2014, opening up the possibility of new services for PAL and the launch of flights to the US by Cebu Pacific. (Cebu Pacific is now preparing to launch services to Guam and Hawaii in early 2015 as Cebu Pacific does not have the aircraft to operate to the mainland US.)

See related report: Cebu Pacific and Philippine Airlines are poised to expand in US following Category 1 upgrade

PAL has been looking at several potential new US destinations including Chicago, Miami, New York and San Diego. But operations to the central or eastern part of the US are challenging because such long flights cannot be operated non-stop without payload restrictions, even with PALs new fleet of 777-300ERs.

One-stop markets can be challenging and are generally better served using partners. Category 1 allows PAL to pursue codeshares in the US market. While it would be difficult to secure a deal with a US major, PAL could find suitable US partners in smaller US carriers such as Hawaiian Airlines, Alaska Airlines, Virgin America and JetBlue.

Hawaiian and Virgin America could be particularly attractive with both potentially providing PAL alternative access to New York (via Honolulu for Hawaiian and via San Francisco and Los Angeles for Virgin America). Hawaiian and Virgin America could also give PAL access to several other mainland US destinations including Las Vegas, which has a large Filipino community.

An expanded partnership with ANA to cover the US market would also be a sensible option. ANA currently serves New York as well as other US markets to which PAL currently does not have any access, including Chicago, Seattle and Washington Dulles.

Partnerships would allow PAL to focus on its existing US destinations and perhaps add one more on the US west coast. Covering the rest of the US market with codeshares would be less risky and allow PAL to better utilise its fleet.

PAL does not have enough efficient long-haul aircraft

PAL has six 777-300ERs, which is only sufficient to cover the existing flights to Los Angeles and San Francisco. PAL currently now serves London and operates some Vancouver flights with inefficient A340s that have an outdated product, including overhead rather than seatback in-flight entertainment monitors in economy. (PALs A330 fleet is used for Hawaii but lacks the range for non-stop flights to the mainland US or Europe.)

PAL recently phased out its 747-400s, which had an even more outdated product. The carrier retained its 747s longer than it wanted due to Category 2 restrictions, which had prevented PAL for six years from changing gauge on any of its US flights.

The 777-300ERs were always intended for US routes and Category 1 gave PAL an opportunity finally to start using the aircraft on the routes they were acquired for. But the rapid phase out of the 747-400s had a negative impact on London and Vancouver as the 777-300ERs had to be freed up for Los Angeles and San Francisco.

PAL has been looking at acquiring additional 777-300ERs. But the airline will need to limit its capital expenditure as it already has committed to renewing its short-haul and medium-haul fleets. PAL should try to replace the A340s before implementing any further expansion of the long-haul network.

The reality is the A340s simply lack the efficiency and product PAL needs to make new long-haul routes viable. San Miguels acquisition of four additional A340-300s in 2013 may have seemed like a good deal as the aircraft came cheap but the operating economics and product represent a step in the wrong direction.

Lucio Tans LT Group takes back PAL

New York as well as other new destinations in the US and Europe were part of an ambitious network expansion strategy under Ramon Ang, the president of San Miguel who has served as president of PAL for the last two years. San Miguel acquired a 49% stake in PAL and PAL Express in Apr-2012 from the LT Group. The LT Group maintained a majority stake but ceded management control to San Miguel.

The original plan was for the LT Group to later sell the remaining stake to San Miguel. But negotiations dragged on for over two years without an agreement. San Miguel in Sep-2014 decided instead to sell back its 49% stake to the LT Group. The deal is expected to be completed within the next few weeks, resulting in Mr Angs formal departure from PAL. In the meantime the LT Group has already regained management control.

While some changes are inevitable, major strategic changes are not expected. The fact New York was confirmed and formally announced after the LT Group regained management control indicates San Miguels network plan is not likely to see major adjustments. The several destinations launched by PAL over the last year will likely be retained and New York will not be the only new destination in 2015.

Under San Miguel, PAL pursued ambitious expansion in the Middle East (with four new destinations), added Toronto (as a tag to Vancouver) and re-entered Europe after a 15-year hiatus. Manila-London Heathrow was launched in Nov-2013 with five weekly flights.

PAL secures better Heathrow slots but still lacks European partner

Heathrow has proven to be a challenging market but PAL's performance in London should improve following an upcoming schedule change made possible by a slot swap. The new flights, which will arrive at Heathrow in the early morning and depart in the late morning, are timed ideally for connections at both ends.

But PAL will not be able to benefit fully from the improved slots unless it secures a European partner. Forging partnerships to cover continental Europe via London as well as potentially via its gateways in the Middle East should be a priority.

The LT Group has a lot on its plate as it takes back control of PAL. In addition to seeking new partnerships, PAL has been aiming to sell a strategic stake.

ANA and Etihad have both ruled out potential investments in PAL at least for the time being. The LT Group could look to re-engage with ANA and Etihad while also exploring other potential suitors that could come to the table with both a comprehensive codeshare partnership and capital.

See related report: Philippine Airlines seeks a strategic investor as its international expansion continues

Finalising the deal with ANA, which was initially negotiated by San Miguel, is a solid first move for the LT Group. But PAL will need a much bigger and stronger portfolio of partners and ideally a strategic partner to be successful in the intensely competitive long-haul market. As PAL becomes more visible in the international market and thus more potentially useful to partners, the quest should grow easier.

Source

Quote Reply

Quote Reply